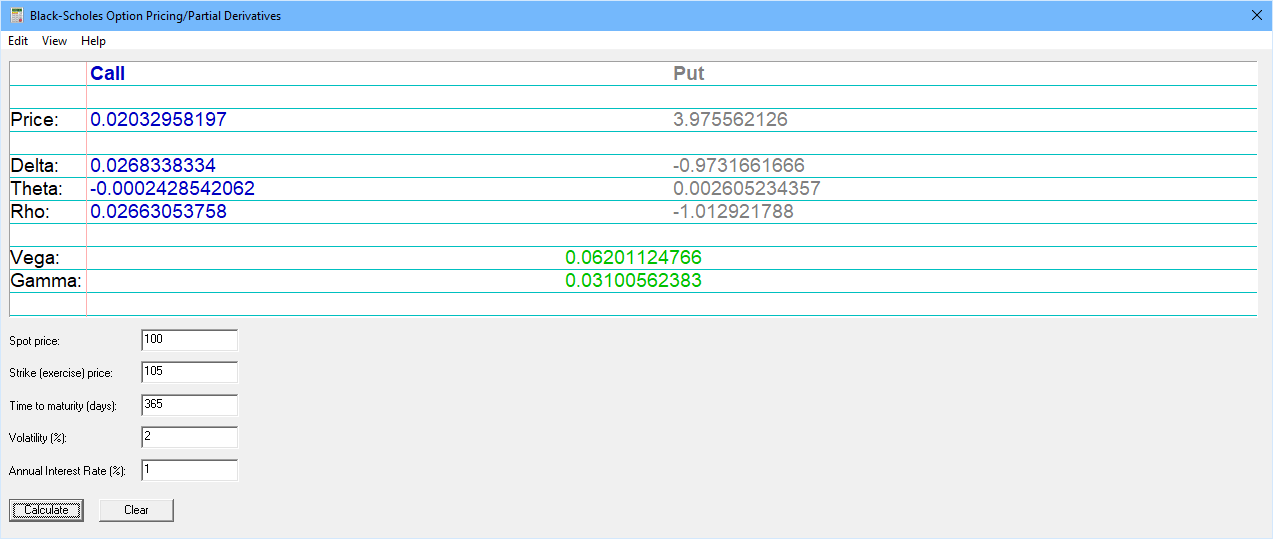

This Black-Scholes Option Pricing Calculator determines the fair market price of European put and call options. It assumes the underlying asset pays no dividends before maturity. We assume no responsibility for the correctness of this software

and it should not be used as a basis for trading decisions. It runs on Windows 10 as a desktop application.

The formulas used are: Call option fair price = S0N(d1) - Xe-rtN(d2) Put option fair price = Xe-rtN(-d2) - S0N(-d1)

on Windows")